The international scientific and analytical, reviewed, printing and electronic journal of Paata Gugushvili Institute of Economics of Ivane Javakhishvili Tbilisi State University

THE IMPACT OF THE DEVELOPMENT OF THE CREDIT DERIVATIVES MARKET ON THE PROCESS OF IMPROVING CREDIT RISK MANAGEMENT IN FINANCIAL INSTITUTIONS

Summary

The development of financial markets since the 1970s has been subjected to increasing globalization. Globalization processes in the area of the international financial system, including the banking sector are becoming increasingly prominent in Poland as well. At present, the immediate source of the global financial crisis of 2008 is associated with the liberalization of the functioning of American investment banks, this is a process that began in the mid-1990s. These banks sold derivative instruments of the subprime type based on income from very risky mortgages. The characteristic feature of derivative instruments is that on this basis it does not occur to sell rights to income or property, as in the case of classical securities, but it happens to resell uncertainty about future market valuation of a financial instrument or other object of a financial market transaction. The emergence of the financial crisis in 2008 indicates the need of improving banking prudential regulations and credit risk management instruments, including the use of derivative instruments. Derivative financial instruments are increasingly used in investment banking to secure credit transactions, which on the one hand is one of the forms of additional collateralisation of the transaction, but also the possibility of generating additional investment risk categories, especially in a situation of a possible decline in economic growth of the domestic or global economy.

Keywords: bank, banking security system, derivative instruments, risk, financial and credit markets, financial crisis, management.

Introduction

Since the end of the 1990s, the development of financial systems has been determined by globalization processes, a benign monetary policy of central banking, an increase in the importance of investment banking and an increased level of volatility in the global economy. In the context of these processes, the importance and scale of the use of derivatives in capital market transactions also increased. By the year 2005, there were few factors that could have led to a significant increase in the credit risk and the financial crisis resulting from it. However, in 2006 - 2008 there is a growing revaluation of investment assets and the importance of speculation is rising on the stock markets (Chisholm, 2013). The breakthrough of these processes is in the autumn of 2008, when the fourth largest Lehman Brothers investment bank collapses and the global financial crisis begins. In order to reduce the dramatic decline in liquidity and lending activities in banking systems, intervention programs were launched to absorb the multimillionaire funds that burden public finances of individual countries. Now, after a decade of the global financial crisis ,optimism has returned to the stock markets again and the economies of most countries are improving their macroeconomic indicators (Fila, Filipiak, 2012).

Despite the significant improvement in the economic growth of the global economy, there are derivatives of the recent financial crisis and not fully solved public debt problems in many countries. Growing lobbying of the financial sector in the governance structures of developed economies results in efforts to activate the economic growth with low interest rates and liberalize lending procedures. After several years of this type of economic processes, these interventions have indirectly contributed to the increased investment and credit risk and to the development of speculative bubbles on stock market exchanges.

The investment banking was perfectly fitted in this process in which financial engineering specialists created new derivative financial instruments. With this aspect of novelty was the possibility of obtaining high profitability based on speculative growth or possibly lower valuations of assets including financial instruments listed on commodity exchanges and stock exchanges. Following this, the process of improving the risk management process should be followed to create similar, new solutions that ensure optimal level of financial system security. In times of a good prosperity, these highly profitable instruments include derivative securities that have grown up ahead of building adequate systems to secure acceptable level of risk (Jajuga, 2009).

Since the economic growth in many countries has been accelerating for several years, the pressure to improve procedural and institutional instruments for credit risk management resulting from derivative transactions may decline. However, this type of decision-makers' approach should not be pursued if the level of overall investment risk in the economy is decreasing as productivity and revenues increase. As a consequence, The Continuation of the improvement of risk management is delayed assuming that the next financial crisis is rather distant. However, it cannot be ruled out that another global or regional financial crisis, such as the European one, will not appear in next years, taking into account, for example, the potential financial insolvency of Greece or Deutsche Bank.

This financial crisis was a result of growing dislocation, the mismatch between the rapid development of derivative instruments, including credit derivatives, and the improvement of credit risk management, including the optimal hedging of transactions. Initially, derivative instruments were used as arbitration for hedging of investment transactions. However, with the development of investment banking and a good prosperity in the stock market, derivative instruments are also being turned into investment products with the high credit risk (Prokopowicz, Dmowski, 2010).

This paper identifies the need to continue the process of improving credit risk management in the context of the derivatives market taking into account the determinants of the risk management process. The descriptive and analytical observation methods were used in this analysis and the results of it will be the basis for the continuation of analyzes undertaken in the field of credit risk management. In the context of analyzes, a research thesis was formulated, which assumed that the post-crisis systemic solutions used so far had stabilized the financial markets but did not fully improve the institutionalized procedures for analyzing and hedging the credit risk of investment banks. It significantly influences on the development of the level of stability of financial systems.

The development of credit derivatives and loan securitization

The development of derivatives markets has begun in the 1970s. During this period there have been already several business cycles and several financial and economic crises with varying degree of influence on the economic processes and the course of globalization of financial markets. Credit derivatives have been used only in the credit risk management process since the early 1990s and are the fastest growing derivatives categories (Pruchnicka-Grabias, 2011, p. 127). The turnover of these instruments is mainly outside the stock exchange, between the financial institutions that are involved. As with interest rate options or foreign exchange rates, credit derivatives reduce credit risk. The bank will receive the amount of the loan agreement for a fee even if the borrower ceases to repeat. In the 1990s, it was widely accepted that the use of derivatives could significantly increase the effectiveness of credit risk management.

The development of credit derivatives in the 1990s is connected with the increase in the deregulation and abolition of formal and institutional barriers on the question of combining classical deposit and credit banking and investment banking. Credit derivatives are used in both classic and active risk management strategies. In classical strategies they are used to completely protect the risk (Suresh, 2014, p. 27).

Active strategies are used to generate additional profits at a certain acceptable level of risk. However, this accepted level of risk was not always adequately protected. Credit derivatives include swap and option contracts that can function throughout the lifetime of the hedged asset or only for a specified period of time (Huterska, 2010, p. At present, the following types of credit derivatives are dominant:

a) income swap transactions,

b) credit default swaps,

c) credit options,

d) debt securities indexed to the loan portfolio.

The development of these financial instruments is determined by many potential uses of these financial transactions in the context of the classical lending business and also in the field of speculative stock market transactions undertaken by some investment banks. Derivative credit instruments are used because of their universal functionality because they allow (Pruchnicka-Grabias, 2011, p. 131):

a) risk management at a relatively low cost,

b) transfer of credit risk to other entities without the need to dispose of hedged assets,

c) obtaining income related to the occurrence of certain credit risk effects.

Currently, most credit derivatives are mainly used to offset the effects of certain credit defaults arising from a single credit transaction or from the loan portfolio. In the portfolio credit risk management process, the derivative instrument can be used to secure the risk arising from (Orzeł, 2012, p. 51):

- the increase in the share of non-performing loans in the loan portfolio,

- from the liquidity reduction of asset refinancing measures.

One of the most important factors in active credit risk management using credit derivatives is the ability to:

- reduction of regulatory capital,

- a change in the credit rating of individual credit assets,

- selling of the risk associated with the customer segment while simultaneously buying risk-weighted assets from other types of borrowers to diversify the risk.

When examining the improvement of credit assessment procedures it is important to take into account changes in this area of credit activity arising from the use of some external rating. Banks that use these methods get an additional source of information about deterioration in creditworthiness, which is to lower the rating of a borrower by a credit rating agency (Wojciechowski, 2009, p. 82).

Using credit derivatives as a form of collateralised transactions in the context of commercial banks' lending activities is also a matter of securitization of loans. Derivative hedging transactions with credit derivatives are undertaken to reduce the risk resulting from the bank's loan portfolio. Since the 1980s, securitization of loans has been developing intensively in foreign banking. Securitization of loans involves the resale of part of credit transactions to another institution in order to change the quality of the loan portfolio.

For a bank to get rid of bad loans, this can be a good solution in comparison to the perspective of the debt collection process. Securitization was first used for mortgages and then it was extended to other types of receivables, such as car loans or receivables from credit cards (Przybylska-Kapuścińska, ed., 2013, p. 83).

Transactions classified as securitization loans allow you to:

a) obtaining cheaper funds beside traditional forms of financing, this is deposits,

b) diversification of funding sources and reduction of risk of liquidity loss,

c) specialization of banks for a specific stage of the lending process,

d) reduction of credit concentration and diversification of loan portfolio,

e) risk spreading through the distribution of issue of securities in tranches with different levels of credit risk,

f) the sale of those types of loans which are fraught with a specific risk category such as the risk of early repayment (Jurkowska-Zejdler, 2008, p. 54).

Looking at the historical background of the financial markets it was noticed that in the international financial markets until the mid 1980s securitization was defined as the issuance of securities as a substitute for bank credit. Later, the meaning of this term was significantly narrowed. The definition of securitization was limited to the issue of securities secured by mortgage or other assets. One of the more synthetic definitions states that securitization is a process in which financial instruments are given the characteristics that enable them to sell in the form of securities (Gwiazdowski, 2012, p. 57). Securitization consists of the following:

a) the economic entity in order to obtain funds distinguishes a package of homogeneous assets,

b) those assets are sold specifically for that purpose in the partnership that is the issuer,

c) the issuer sells securities that have previously been subjected to a credit rating by credit rating agencies.

It also happens that securitization may be the only way to raise funds. The company that is negatively assessed by the bank will not receive a loan. However, if the company has unpaid receivables from the highest rated institution, then the management of the bank may choose to carry out a securitization.

The impact of the global financial crisis of 2008

on the development of the derivatives market

Therefore, in recent years, the development of national systems and global financial markets has been modeled on the high level of volatility in the global economy, which is a derivative of the recent financial crisis and not fully solved public debt problems in many countries. Governments attempted to boost economic growth indirectly and these attempts contributed to the increased investment and credit risks and to speculative bubbles on capital markets. In this process, investment banking was a perfect investment in which financial engineering specialists invented new financial instruments (Domańska-Szaruga, 2013).

The aspect mentioned above was related to the possibility of obtaining high profitability based on speculative growth or possibly falling valuations of assets, including financial instruments listed on commodities and stock exchanges. Following this, the process of improving the risk management process should be followed to create similar, new solutions that provide the optimum level of financial system security. In good times of prosperity, these highly profitable instruments include derivative securities, which have anticipated building adequate systems to secure acceptable levels of risk. The recent financial crisis was a result of growing dislocation and the mismatch between the rapid development of derivative instruments, including credit derivatives and the improvement of the credit risk management process underlying transactions based on these instruments (Prokopowicz, Dmowski, 2010).

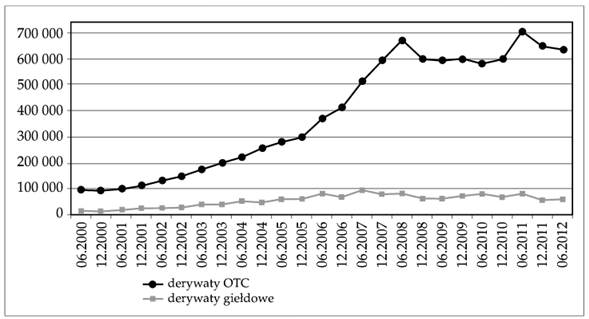

Now, after that financial markets have returned to the financial equilibrium and economic growth improves after the post-crisis slowdown, more data are available. These data allow for an objective assessment of the correlation in the development of derivative markets, including transactions involving credit derivatives and the cyclical nature of the global economy and the development phase of the stock markets. Before the financial crisis in 2008, the financial derivative market was one of the most rapidly growing financial markets on a global scale. The high rate of this growth is shown in the chart below. It is clear from this figure that OTC market is clearly an over-the-counter segment of this market. On the other hand, transactions in the stock exchange segment are entered into much lower amounts.

Figure 1. Derivative financial instruments market in 2000-2012 (USD billion).

Source: BIS Quarterly Review, Bank for International Settlement, reports for December 2001 - September 2012 (www.bis.org).

The need to investigate potential determinants of the source of the financial crisis has drawn the attention of economists to the issue of strengthening supervisory institutions and supplementing regulation in order to better align them to the level of development of the derivatives market. On the other hand, there is a prevailing opinion that arguments for the need of introducing appropriate regulations are not intended to limit the free market-trading of financial markets and the introduction of manual control of these markets by the government (Zygierewicz, 2007, p. 14). The improvement of these regulations should take into account the improved functioning of the market mechanism so that all participants in the market have more symmetrical access to information that may be useful in making decisions relating to the investment in derivatives and that they are fairly informed about the market.

Where this risk is relatively high, financial supervision should organize and control the mechanisms that mitigate them ,for example obliging sellers of financial instruments to honestly inform and warn investors of the risks they accept. In addition, normative regulations should take into account the expansion of the system of special-purpose reserves created to cover possible losses, this is an analogous system that has been in operation for decades for bank loans. The high level of significance of this issue highlights the fact that despite the financial crisis, which emerged in 2008, some segments of the derivatives market still show a strong tendency to increase the value of transactions (Gwoździewicz, Prokopowicz, 2015, p. 156).

The need for a permanent process of improving banking regulations, adapting them to changing market conditions and strengthening the role of prudential instruments of supervisory institutions also applies to financial markets operating in Poland. However, the significance of this issue was relatively small due to the investment banking that does not exist in Poland in such form and size as it is in highly developed countries, especially in the USA. However, in the context of the strengthening of prudential instruments in Western European banking systems, eg in the field of banking guarantee systems, analogous measures to increase the level of system security were also implemented in Poland.

The global financial crisis of 2008, which direct source was the speculative bubble of instruments based on subprime bonds, is just one of the key aspects of the problem of the ended crisis. The financial crisis has been effectively controlled but its source has not been completely eliminated. Increasing the capital requirement to cover the risks borrowed by a bank of debt securities is not enough to maintain financial stability in banking systems. The process of globalization, deregulation in the financial markets, mergers and acquisitions in the financial market, the activity of hedge funds, merging of classical deposit and credit banking with investment are just some aspects at the macro level that have played a role in the growth of credit risk in financial markets (Niedziółka, 2011, p. 71). Therefore, there are many aspects of credit risk management that require further investigation and successive refinement to ensure these transactions are more secure.

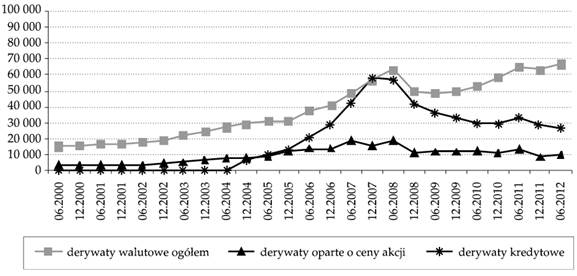

The dynamic growth of the derivative financial instruments market against other derivatives market segments preceding the appearance of the financial crisis in 2008 is presented in the chart below. Attention is also paid to the relatively large decrease in transactions in derivative credit instruments following the emergence of the mentioned financial crisis.

Figure 2. Derivative market for currency, credit and equity-based instruments in 2000-2012 (USD billion).

Source: BIS Quarterly Review, Bank for International Settlement, reports for December 2001 - September 2012 (www.bis.org).

Therefore, it is crucial to clarify the nature of credit risk management in the context of the derivatives market with an analysis of the determinators shaping the management process. During this analysis, descriptive and analytical methods of analysis were applied. The results of this analysis will be the basis for the continuation of analyzes undertaken in the area of credit risk management. The observation method and critical analysis were applied to the key issues discussed in this paper on the issue of credit risk management process and the role of derivatives in the context of increasing risk in financial markets.

In the context of the analyzes, a research thesis has been adopted. It assumes that the post crisis, systemic solutions have not fully improved the institutional procedures for analyzing and hedging credit risk transactions and these solutions do not ensure optimal levels of financial stability (Domańska-Szaruga, 2014).

Summary

The discussions confirm the continuation and the need to permanently improve the credit risk management process for transactions involving financial derivative instruments. Significant improvement of the global economic situation and domestic economies does not slow down the continuation of this process. In this paper, the research hypothesis is based on the assumption that the existing systemic solutions have stabilized the financial markets but have not fully improved the institutional procedures for analyzing and hedging the credit risk of investment banks, which significantly influences on the stability level of financial systems. The thesis mentioned above was confirmed on the basis of analyzes conducted in financial institutions, the solutions related to the improvement of credit risk management instruments.

Almost a decade has passed since the global financial crisis and many point to the fact that economic growth is becoming a lasting trend and investors have already forgotten the dangers that cannot be ruled out in the capital markets. Therefore, central institutions in commercial and public financial systems should continue the process of improving credit risk management and investigate potential risks arising from the use of derivatives in transactions undertaken primarily by investment banking. Many central banks still maintain very low interest rates despite the lack of expected growth in business and enterprise development.

Credit rating agencies continue to give their credit rating recommendations on a variety of occasionally modified criteria. As a result, there is still a strong pressure to improve credit risk management procedures, including in the derivatives market and the use of these instruments in loan business. At present, risk management system are requiring the system and institutional refinement, particularly in the area of improving the acceptable level of risk instruments for investment banking transactions. Supplementation require prudential procedures to reduce the incongruity between the use of derivatives in highly profitable investment banking operations and the applied safeguards for acceptable levels of risk since the 1990s.

The global financial crisis, which has been the direct source of speculative bubble of subprime-based instruments, is a major global financial crisis forgotten by capital market participants. It is only one of the key aspects of the ended crisis. It is being assumed that the global financial crisis of 2008 has been effectively controlled, but its source has not been fully eliminated. Increasing the capital requirement to cover the risks borrowed by a bank of debt securities is not enough to maintain financial stability in banking systems.

Processes of globalization, deregulation, mergers and acquisitions in the financial market, the activity of hedge funds, merging of classical deposit and credit banking with investment are just some aspects at a macro level which have played a special role in growth credit risk on financial markets. As a result, there are many aspects of credit risk management that require further investigation and successive refinement to ensure that transactions are more secure (Niedziółka, 2011).

It is also important to improve the safety of the financial system and to reduce the risks not only at the level of sales of financial instruments and at the transaction level but also to coordinate the processes of improvement of the instruments of systemic risk management by the central institutions of financial systems. For example, issues such as the transparency of the central bank's stability policy, methods of quantifying and hedging systemic risk, recommendations of credit rating agencies, performance of national and supra-national financial market supervisors are further key aspects in the context of the modeling of credit risk management systems that require successive improvement their performance to develop stable, resistant to crisis financial systems.

In addition, the process of improving credit risk management should be also continued in analytical and sales operation and in information flows, especially in terms of risk estimation and the establishment of adequate risk hedging for individual financial transactions. The banks themselves fail to ensure that financial systems are stable, as well as relevant national central banking and international financial stability initiatives are needed.

References:

- BIS Quarterly Review (2012), Bank for International Settlement, Reports for December 2001 - September 2012, (www.bis.org).

- Chisholm A. M. (2013), Wprowadzenie do międzynarodowych rynków finansowych, Warszawa: Wydawnictwo Wolters Kluwer.

- Domańska-Szaruga B. (2014), Financial Instability and the New Architecture of Financial Supervision in European Union (in:) Domańska-Szaruga B., Stefaniuk T. (red.), Organization in changing environment. Conditions, methods and management practices, Warszawa: Wydawnictwo Studio Emka.

- Domańska-Szaruga B. (2013), Common banking supervision within the financial safety net, (in:) The Economic Security of Business Transactions. Management in business, Oxford: Wydawnictwo Chartridge Books Oxford.

- Fila J., Filipiak B. (2012), System finansowy a rozwój gospodarczy. Szanse i zagrożenia, Warszawa: Wydawnictwo Difin.

- Gwiazdowski R. (2012), A nie mówiłem. Dlaczego nastąpił kryzys i jak najszybciej z niego wyjść?, Warszawa: Wydawnictwo Prohibita.

- Gwoździewicz S., Prokopowicz D. (2015), Importance and implementation of improvement process of prudential instruments in commercial banks on the background of anti-crisis socio-economic policy in Poland (in:) Globalization, the State and the Individual, “International Scientific Journal”, Free University of Varna “Chernorizets Hrabar”, Chayka, Varna, Bułgaria 9007, Varna 2015, nr 4(8) 2015.

- Huterska A. (2010), Kredytowe instrumenty pochodne w zarządzaniu ryzykiem kredytowym, Warszawa: Wydawnictwo CeDeWu.

- Jajuga K. (2009), Instrumenty pochodne. Anatomia sukcesu. Instytucje i zasady funkcjonowania rynku kapitałowego, Komisja Nadzoru Finansowego, Warszawa: Wydawnictwo CEDUR.

- Jurkowska-Zejdler A. (2008), Bezpieczeństwo rynki finansowego w świetle prawa Unii Europejskiej, Warszawa: Wolters Kluwer,.

- Niedziółka P. (2011), Kredytowe instrumenty pochodne a stabilność finansowa, Warszawa: Wydawnictwo SGH.

- Orzeł J. (2012), Zarządzanie ryzykiem operacyjnym za pomocą instrumentów pochodnych, Warszawa: Wydawnictwo Naukowe PWN.

- Prokopowicz D., Dmowski A. (2010), Rynki finansowe, Warszawa: Wydawnictwo Centrum Doradztwa i Informacji Difin sp. z o.o.

- Pruchnicka-Grabias I. (2011), Pochodne instrumenty kredytowe. systematyka, wycena, zastosowanie, Warszawa: Wydawnictwo CeDeWu.

- Przybylska-Kapuścińska W. red. (2013), Funkcjonowanie współczesnego rynku pieniężnego i kapitałowego, Warszawa: Wydawnictwo CeDeWu.

- Suresh S. (2014), Papiery wartościowe o stałym dochodzie i instrumenty pochodne, Seria Finanse i Inwestycje, Warszawa: Wydawnictwo Wolters Kluwer.

- Wojciechowski J. (2009), Rynek giełdowych finansowych instrumentów pochodnych w Polsce. Rys historyczny, stan obecny i perspektywy, Warszawa: Wydawnictwo GPW.

- Zygierewicz M. (2007), Zarządzanie kryzysowe w bankowości europejskiej – definicja problemu i aktualny stan prawny, Studia i Prace Kolegium Zarządzania i Finansów, Zeszyt Naukowy 77, Warszawa: Wydawnictwo Szkoła Główna Handlowa w Warszawie.